If you own your home, your mailbox is a battlefield. Every week, you likely receive envelopes with bold red letters shouting “NOTICE OF ELIGIBILITY” or “GOVERNMENT BACKED CASH SETTLEMENT.” Some even feature the Great Seal of the United States or logos that look suspiciously like the Department of Housing and Urban Development (HUD).

For a senior looking for Debt Relief, these letters look like a legitimate lifeline. But for many, they are “Data Traps” designed to harvest your Social Security number and equity information to be sold to high-pressure boiler rooms.

But here is the sageWISE Warning: The government does not send out mass mailers to “offer” you a Reverse Mortgage. HUD and the FHA insure the loans, but they never market them directly to you.

As your trusted advocate, we have performed a Sagewise Audit of the 2026 predatory marketing landscape. We will show you the three most common “Anxiety Hooks” used by scammers, how to vet a lender in 60 seconds, and the one “Fee” you should never pay.

Key Takeaways

- The Logo Trap: Legitimate FHA/HUD logos on a mailer do not mean the mailer is from the government.

- Free Information: You should never pay for an “Eligibility Report” or a “Benefits Guide.” These are free from any reputable lender.

- The Celebrity Factor: Just because a famous actor or politician is the spokesperson doesn’t mean the loan officer in the office is acting in your best interest.

- The sageWISE Tip: If a caller pressures you to “sign today” to lock in a rate before a “deadline,” hang up. A Reverse Mortgage requires a mandatory counseling session by law.

Don’t get trapped by a data predator. See if you qualify through a verified, safe process.

Check Your Reverse Mortgage Eligibility Now

The sageWISE Audit: The "Government Fake-Out"

Predatory marketers use “Borrowed Authority” to lower your guard. They want you to believe that the government—not a private sales company—is recommending their specific product.

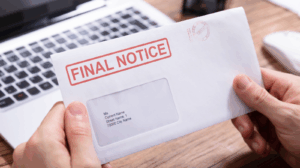

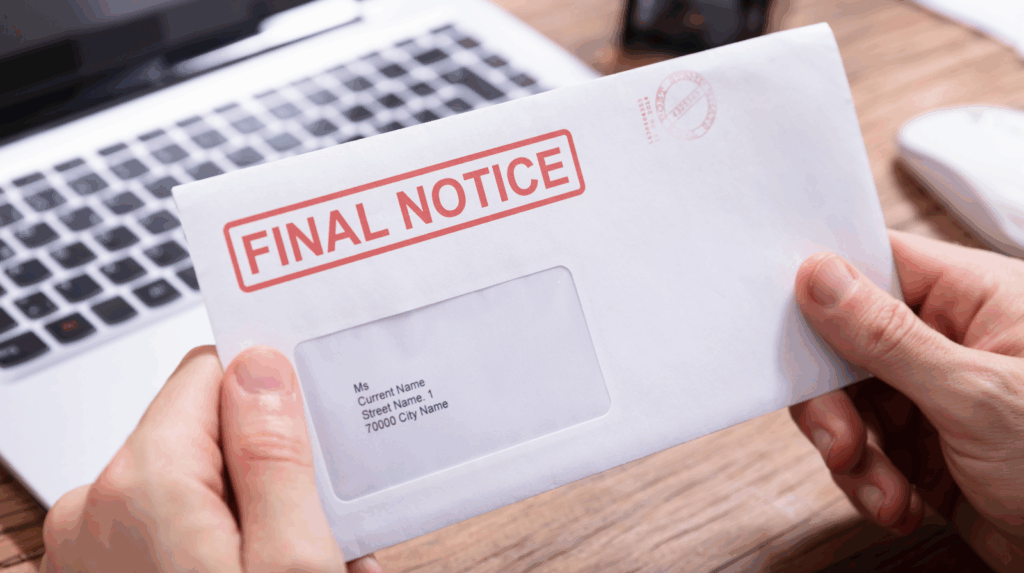

1. The Fake HUD Letter

The letter arrives in a “brown paper” envelope or features a barcode and a fake “Case Number” to look like a tax document or a Social Security update.

- The Tactic: Forced Urgency. The letter will state you have a “Deadline to Claim Your Equity” or that your current mortgage is “At Risk for Liquidation.” These are lies intended to trigger a panic-driven phone call.

- The Reality: These companies buy “Trigger Leads” from the credit bureaus. If you recently checked your credit score or looked at a mortgage site, they know you are in the market. The “Case Number” is usually just your public parcel ID from the county records office.

- The Shield: Check the return address. If it doesn’t end in an official Washington, D.C. zip code or isn’t from the “U.S. Department of Housing and Urban Development,” it’s a solicitation. Legitimate FHA disclosures include a specific disclaimer at the bottom in tiny print: “Not affiliated with any government agency.” If that disclaimer is missing, the company is violating federal advertising laws.

2. The "Senior Benefits" Specialist

You receive a call from someone with a calm, professional voice claiming to be a “Federal Housing Auditor” or an “Equity Counselor.”

- The Tactic: The Fake Survey. They start by asking “verification questions” like your age, your home value, and your current mortgage balance. They claim they are checking to see if you “qualify for the 2026 Senior Relief Grant.”

- The Reality: They are Lead Generators. They do not buy houses or issue loans. Once they harvest your data, they sell your “profile” to five different high-pressure mortgage companies. Within an hour, your phone will start ringing with aggressive salespeople who will harass you for weeks.

- The sageWISE Move: As we noted in our Stop the Spam guide, never confirm your Social Security number or date of birth to an inbound caller. Tell them: “I am on the National Do Not Call Registry. If you call again, I will file a report with the FTC.” Then hang up.

Quick Comparison: A Vetted Lender vs. A Data Trap

|

Feature

|

Vetted sageWISE Lender

|

Predatory Data Trap

|

|---|---|---|

|

Initial Contact

|

You initiate the quote on your terms.

|

High-pressure cold calls or texts.

|

|

Documentation

|

Provides an FHA "Guide to Benefits."

|

Asks for your SSN in the first 2 minutes.

|

|

Counseling

|

Insists on independent HUD counseling.

|

Tells you counseling is "a waste of time."

|

|

Branding

|

Transparent private company name.

|

Uses names like "Federal Relief Center."

|

|

Pressure Level

|

Consulting and educational.

|

"Sign today to lock in the deadline."

|

|

Fees

|

Disclosed on an official Loan Estimate.

|

Asks for "Upfront Processing Fees."

|

The "Spokesperson" Mirage: Logic vs. Celebrity

Reverse mortgage companies spend tens of millions on celebrity spokespeople—usually trusted actors or former politicians who built a career playing “honest” and “heroic” characters.

- The Psychology: Parasocial Trust. You have “known” these actors for 40 years through your TV screen. Marketers count on you transferring that trust to the loan. They want you to feel that “The Actor” has vetted the loan for you.

- The Reality Check: The celebrity is a paid endorser. They are often paid per commercial or receive a percentage of the lead volume they generate. They are not financial advisors, they aren’t in the room when you sign the Non-Recourse Shield documents, and they won’t be there to help your heirs when the loan becomes due.

- The Bodyguard Advice: Ignore the friendly face on the TV and focus on the Annual Percentage Rate (APR) and the Closing Costs. A celebrity-endorsed loan can still carry an interest rate that is 1% higher than a less-advertised, vetted competitor. Always ask for a side-by-side comparison of the “Celebrity Brand” vs. a standard FHA HECM.

How to Vet a Lender in 3 Steps

Before you give your address or financial details to anyone, perform this digital “Financial Bodyguard” audit:

- Check the NMLS Number: Every legitimate loan officer in the U.S. is assigned a permanent NMLS ID. By law, this number must be on every mailer and website. Go to NMLSConsumerAccess.org and type in the number. Look for the “Regulatory Actions” section. If the company has a history of state fines or the officer has a history of disciplinary issues, do not do business with them.

- Verify the “HUD Counseling” Protocol: Federal law requires that you speak to an independent, third-party counselor before you can even apply for a HECM. If a lender tries to suggest a “preferred” counselor or tells you they can skip this step, they are attempting to manipulate you. A legitimate lender will provide you with a list of 10+ different government-approved agencies and tell you to pick one yourself.

- The “Upfront Cash” Rule: A legitimate lender will never ask you to pay them cash upfront (via Zelle, wire, or check) for a “Credit Review” or a “Retainer.” The only fee you should pay before closing is the cost of the Appraisal, which you should pay directly to the appraisal company or through a secure, transparent portal—not a salesperson.

Home Equity “Cash Unlock” Calculator

Avoid the “Data Trap” by running your own numbers first. Use our Home Equity Calculator to see your estimated “Principal Limit” based on your age and home value before you talk to a single salesperson.

Frequently Asked Questions (FAQ)

No, not directly. However, if they trick you into signing a “Subject To” agreement, they can steal your deed. A Reverse Mortgage requires a formal closing with a title company, making it much harder for a total fraud to happen—but the “scam” is usually in the high fees and bad advice, not the loan itself.

As we noted in the Inherited Property Sharks guide, scammers monitor death notices. They assume a surviving spouse is vulnerable. This is the most important time to rely on your Spousal Protection Rule knowledge and ignore the junk mail.

No. Any company charging you to “check your eligibility” is scamming you. Qualifying is a standard part of the sales process and should always be free.

Yes. Reverse mortgages are much more lenient than traditional loans. If someone tells you that you need to pay a “Credit Repair” fee to get a HECM, they are likely trying to steal your money.

Take a photo of the mailer and send it to the Federal Trade Commission (FTC) or your state’s Attorney General. You can also report them to the Better Business Bureau (BBB).

Check Your Reverse Mortgage Eligibility Now (Get facts from vetted sources. Protect your home and your data today.)