It is the question every parent asks themselves, usually in the middle of the night: “If I pass away with a balance on my credit card, will my children be forced to pay it?”

The fear of burdening your loved ones is real. Debt collectors often prey on this fear, calling grieving families and demanding payment for debts they do not legally owe.

As your trusted advocate, we are here to give you the clear, legal truth. In most cases, your children are NOT responsible for your credit card debt.

However, there are exceptions. This guide will explain exactly how debt is handled after death, how to protect your heirs from aggressive collectors, and how to ensure your estate is set up correctly.

Key Takeaways

- The Golden Rule: Unsecured debt (like credit cards) usually dies with you. Your heirs are not personally liable unless they co-signed.

- The “Estate” Pays: Creditors can ask for payment from your estate (your assets), but they cannot come after your children’s personal money.

- Authorized Users are Safe: An authorized user is not liable for the debt. A joint account holder is.

- Life Insurance is Protected: Your life insurance payout generally bypasses the estate and cannot be touched by credit card companies.

The Law: Who Is Actually Responsible?

1. The Estate’s Job Your estate is the collection of everything you own (bank accounts, car, home) at the time of death. The executor of your will uses these assets to pay off any outstanding debts.

- If there is money: The estate pays the credit card bill. Your heirs get whatever is left over.

- If there is NO money (Insolvent Estate): If your debts are bigger than your assets, the estate is “insolvent.” The credit card company must write off the loss. They cannot legally ask your children to pay the difference.

2. The Co-Signer Exception (The Risk) If you have a Joint Account Holder or a Co-Signer on the card (like a spouse or child), that person is 100% responsible for the debt immediately.

- Note: This is different from an “Authorized User.” An authorized user (someone you just gave a card to) is never responsible for the debt.

Protecting Your Family: 3 Steps to Take Now

You can take action today to ensure your debt doesn’t cause a headache for your heirs.

1. Check Your “Authorized Users” Go through your cards. If you added a child or grandchild as an authorized user,

make sure they know they are not liable. If you are worried about confusion,

remove them from the account now.

2. Designate Beneficiaries (The “Bypass” Strategy) Creditors can only go after assets in your probate estate.Assets with a named beneficiary bypass probate and go directly to your loved one,safe from creditors.

- Action:

Ensure your Life Insurance, 401(k), and IRA all have named beneficiaries.

- Action:

3. Leave a “Digital Wallet” File Your executor needs to know what cards you have so they can close them quickly to prevent fraud. Make a list of your open credit cards and customer service numbers and keep it with your will.

The "Debt Collector" Warning for Heirs

If you are an heir reading this, be warned: Debt collectors will try to trick you.

They may call and say, “You need to pay your mother’s bill out of moral obligation,” or implying you are legally required to.

Your Script:

“I am the executor of the estate. All debts will be paid from the estate’s assets in accordance with probate law. Do not contact me personally about this debt again.”

Under the Fair Debt Collection Practices Act (FDCPA), they cannot harass you or mislead you about your liability.

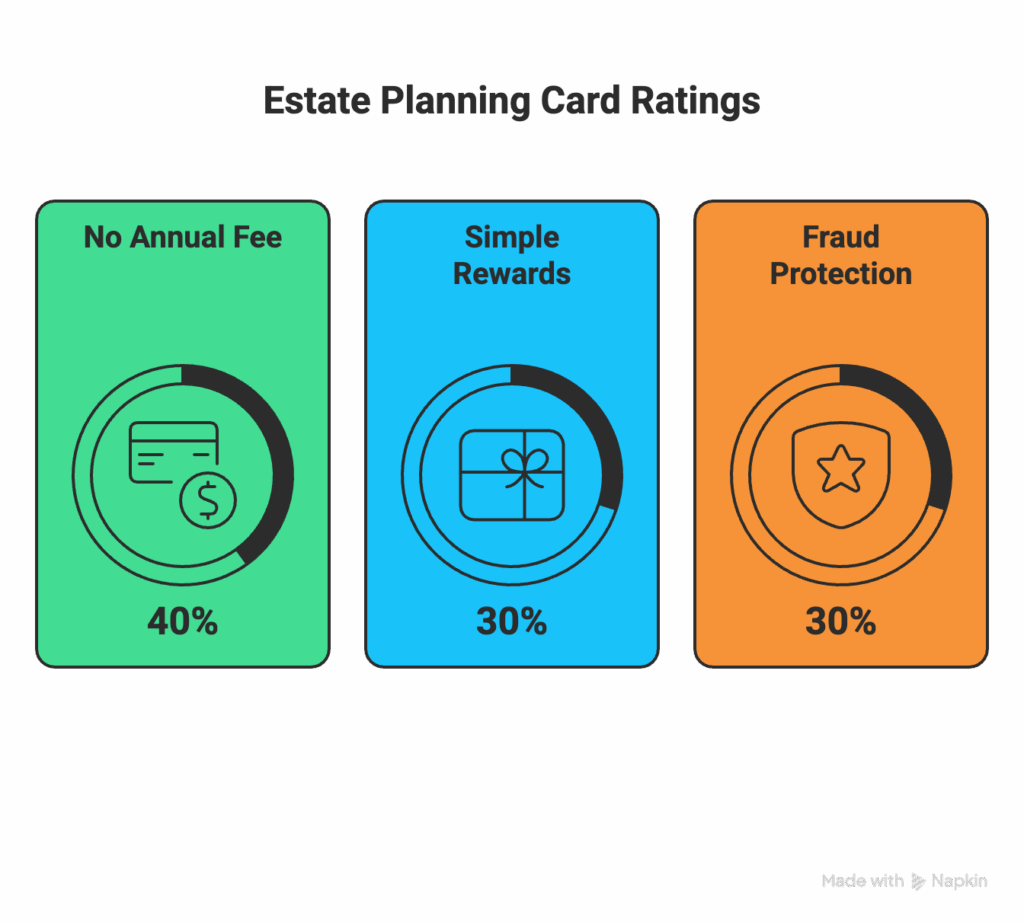

How We Rate Cards for Estate Planning

- No Annual Fee (40%): We prioritize cards that cost nothing to hold, so your estate isn’t drained by fees if closing the account takes time.

- Simple Rewards (30%): We look for flat-rate cash back that can be redeemed easily, ensuring you don’t leave value on the table for the bank to reclaim.

- Fraud Protection (30%): We only recommend cards with $0 Fraud Liability, protecting your estate from identity theft after you pass.

Top Picks: Cards That Help You Simplify

If you are organizing your finances for the future, simple is better. Moving to a single, no-fee card makes life easier for you and your executor.

Best Estate-Friendly Cards at a Glance

|

Redemption Method

|

Best For

|

Key Benefit

|

|---|---|---|

|

SoFi Unlimited 2%

|

Simplicity

|

Flat 2% cash back + $0 Fraud Liability.

|

|

Indigo Platinum

|

Rebuilding

|

Unsecured card for less-than-perfect credit.

|

|

Milestone Mastercard

|

Access

|

Easy approval for limited credit profiles.

|

1. Best for Simplicity: SoFi Unlimited 2% Credit Card

Sagewise Rating: 5.0

- Why it wins:

It has No Annual Fee, earns a flat 2% cash back, and has $0 Fraud Liability.

It is a simple, clean account that is easy to manage and easy to close if needed.

The 2% cash back is automatically deposited, meaning your rewards are never “lost”

in a confusing points portal.

View Offer

2. Best for Rebuilding (If Debt is High): Indigo Platinum Mastercard®

Sagewise Rating: 4.0

- Why it wins:

If you are struggling with debt now, this unsecured card helps you maintain access

to credit without a security deposit, allowing you to keep your cash liquid for your estate.

It reports to all three credit bureaus, helping you rebuild your score to qualify for

better rates on other loans.

Check Pre-Approval

3. Best for Limited Credit: Milestone Mastercard®

Sagewise Rating: 4.0

- Why it wins:

If your credit profile is limited, Milestone offers a path to an unsecured card

without a deposit. It simplifies your finances by giving you a single, manageable

credit line that reports to major bureaus, helping you establish a clean financial

record for your estate.

Apply Now

Frequently Asked Questions (FAQ)

It is possible, but rare. If your estate has no cash but owns a house, creditors can file a claim against the estate, forcing the house to be sold to pay the debt. However, many states have Homestead Exemptions or laws protecting a surviving spouse’s right to live in the home.

It depends on where you live. In Community Property States (like California, Texas, Arizona), debts incurred during the marriage are generally considered joint debts, and your spouse could be liable. In Common Law States, your spouse is generally not liable unless they co-signed.

As we discussed in our Rewards Guide, most points expire immediately upon death. It is best to redeem your cash back monthly so the value sits safely in your bank account.

Usually, no. These “credit protection” plans are expensive and have many loopholes. A standard Final Expense Life Insurance policy is a much cheaper and more reliable way to ensure your debts are covered.

Every state has a “probate window” (often 3 to 6 months after notice is published). If a credit card company does not file a claim against the estate within that window, they lose the right to collect forever.

Find the Best Credit Card Rates (Ensure your financial legacy is secure. Compare cards today.)