While hospital payment plans are the traditional route for handling medical debt, a 0% APR credit card is often the superior financial tool for seniors. It offers total flexibility on monthly payments, a longer repayment window (often up to 21 months), and the ability to earn cash back on the bill—benefits that rigid hospital plans simply cannot match.

You’ve just received a large medical bill—maybe for a surgery, dental work, or a hospital stay not fully covered by Medicare. The total is $2,000, $5,000, or more.

Your first instinct might be to call the hospital and set up a monthly payment plan. It seems like the responsible thing to do.

But before you sign that agreement, you need to know your options. Hospital payment plans can be rigid, and if you miss a payment, the consequences can be severe.

As your trusted advocate, we are here to show you why using a 0% card gives you more control, better cash flow, and a smarter way to clear your debt.

Key Takeaways

- The Hospital Trap: Payment plans are often inflexible. If you miss one, they can send you to collections immediately.

- The 0% Advantage: A 0% APR card acts as an interest-free loan for 15-21 months, giving you total control over how much you pay each month.

- The Bonus: You can earn 2% cash back on the medical bill, effectively giving yourself a discount on the procedure.

- The Strategy: Put the bill on the card, then set up your own payment plan to clear it before the 0% rate expires.

Option 1: The Hospital Payment Plan

- Pros: It is usually interest-free (0%) if you pay it off quickly.

-

Cons:

- Inflexible: You must pay the agreed amount every month. You can’t skip a month if you have an emergency.

- Aggressive Collection: If you miss a payment, the hospital can demand the full balance immediately or send it to a collections agency, which hurts your credit score.

- No Rewards: You get nothing back for paying thousands of dollars.

Option 2: The 0% APR Credit Card (The Smarter Tool)

- Pros:

- Total Flexibility: You decide how much to pay each month. If you have a tight month, you can pay the minimum. If you have extra cash, you can pay more.

- Longer Terms: You often get 18+ months to pay it off, which might be longer than the hospital offers.

- Cash Back: Most cards offer 1.5% to 2% cash back. On a $5,000 bill, that’s $100 back in your pocket.

- Safety: The hospital is paid in full. They can’t send you to collections because you don’t owe them anything anymore.

Side-by-Side: Paying a $5,000 Medical Bill

Let’s compare the two strategies for a $5,000 surgery bill.

|

Feature

|

Hospital Payment Plan

|

0% APR Credit Card

|

|---|---|---|

|

Monthly Payment

strong>

|

Fixed ($416/mo for 12 months)

|

Flexible (Min. $50 - You Choose)

|

|

Interest

|

0%

|

0% (for 15-21 months)

|

|

Missed Payment?

|

Sent to Collections immediately.

|

Late fee, but debt stays with the bank.

|

|

Rewards Earned

|

$0

|

$100+ Cash Back

|

|

Your Status

|

"In Debt to Hospital"

|

"Paid in Full"

|

How to Execute This Strategy

- Check Your Credit: You generally need a score of 670+ to qualify for the best 0% APR cards.

- Find the Right Card: Look for a card with the longest 0% intro period (15+ months) and no annual fee. (See our top picks below).

- Pay the Bill: Use the card to pay the medical provider in full. Ask for a receipt showing a $0 balance.

- Set Your Own Plan: Calculate your monthly payment: (Total Bill) ÷ (Months of 0% APR). Set up auto-pay for this amount to ensure you are debt-free when the promo ends.

Top Picks: Best Cards for Medical Bills

If you have good credit, these cards are excellent tools for managing medical costs. Use this table to find the right fit for your situation.

Quick Look: Best Cards for Medical Expenses

|

Card Name

|

Best For

|

Intro APR Period

|

Key Benefit

|

|---|---|---|---|

|

Wells Fargo Reflect®

strong>

|

Longest Payoff

|

Up to 21 Months

|

Maximum time to pay interest-free.

|

|

SoFi Unlimited 2%

|

Cash Back Offset

|

Standard Promo

|

2% Cash Back reduces your total bill cost.

|

|

Citi Simplicity®

|

Peace of Mind

|

Up to 21 Months

|

No Late Fees ever, preventing mistakes.

|

|

Chase Freedom Unlimited®

|

Prescriptions

|

15 Months

|

3% Cash Back at drugstores for ongoing meds.

|

|

Citi® Diamond Preferred®

|

Low Rates

|

"In Debt to Hospital"

|

"Paid in Full"

|

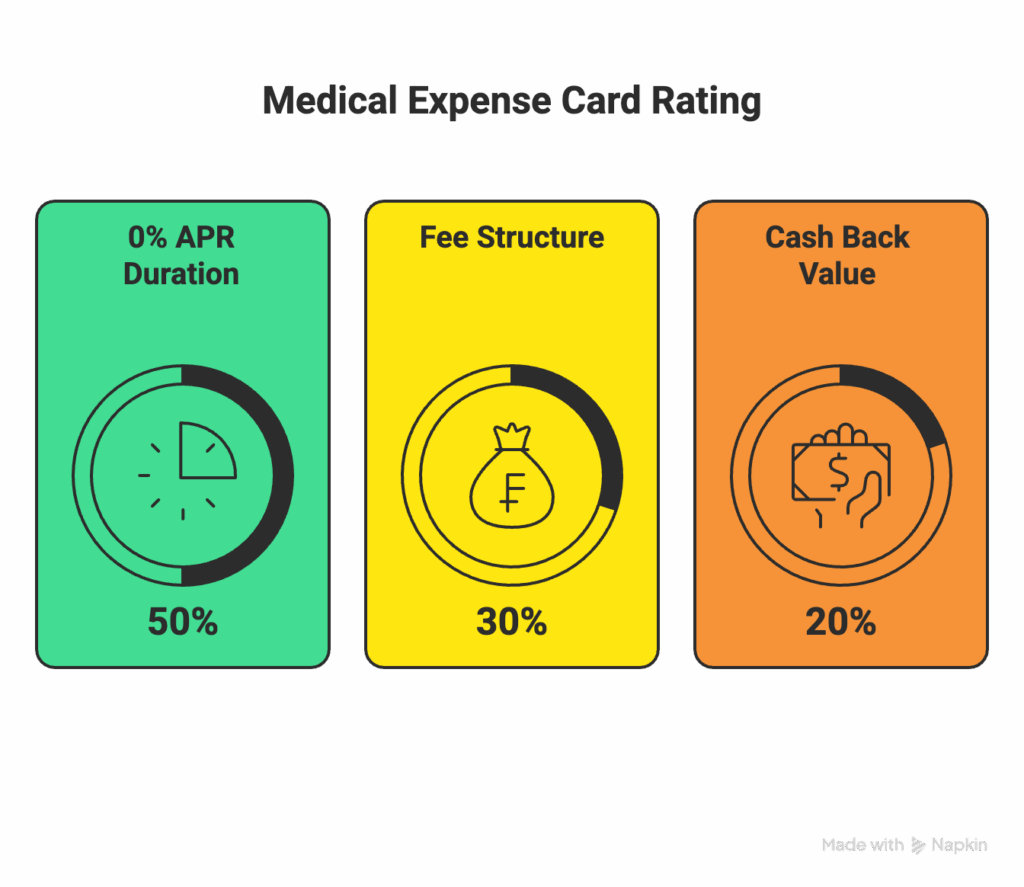

How We Rate Cards for Medical Expenses

- 0% APR Duration (50%): This is the most critical factor. The longer the 0% period (e.g., 21 months vs. 12 months), the smaller your required monthly payment will be.

- Fee Structure (30%): We prioritize cards with No Annual Fee. You shouldn’t have to pay to carry the card. We also look for cards with No Late Fees to protect you from accidents.

- Cash Back Value (20%): While secondary to the 0% rate, earning cash back effectively lowers the cost of your surgery or device. A card that gives 2% back is an instant 2% discount on your bill.

1. Best for Long Payoff: Wells Fargo Reflect® Card

Sagewise Rating: 5.0

- Why it wins:

It offers one of the longest 0% intro APR periods on the market (up to 21 months

with on-time payments). This gives you nearly two years to pay off a surgery interest-free.

View Offer

2. Best for Cash Back: SoFi Unlimited 2% Credit Card

Sagewise Rating: 5.0

- Why it wins:

You get an unlimited 2% cash back on the medical bill. For a large procedure like a

$5,000 dental implant, that is $100 back in your pocket immediately.

Plus, it has No Annual Fee, making it a great card to keep long-term.

View Offer

3. Best for Peace of Mind: Citi Simplicity® Card

Sagewise Rating: 4.5

- Why it wins:

This card is famous for being “forgiving.” It has No Late Fees,

No Penalty Rate, and often offers a massive 21-month 0% APR

period on transfers and purchases. If you are worried about forgetting a payment during

recovery, this card protects you from penalties.

View Offer

4. Best for Ongoing Meds: Chase Freedom Unlimited®

Sagewise Rating: 4.5

- Why it wins:

While it offers a solid 15-month 0% APR period, its real power is the

3% Cash Back at Drugstores. If your medical bill involves expensive monthly

prescriptions or supplies from CVS or Walgreens, this card continues to save you money

long after the surgery is paid off.

View Offer

5. Best for Low Interest: Citi® Diamond Preferred® Card

Sagewise Rating: 4.0

- Why it wins:

Similar to the Simplicity card, this offers a huge 21-month 0% APR window.

What sets it apart is that it is designed to have one of the lowest ongoing interest rates

after the promotion expires, making it a safer landing spot if you can’t quite

pay off the full balance in time.

View Offer

Frequently Asked Questions (FAQ)

Maybe. Some providers charge a 2-3% “processing fee” for credit cards. Ask first. If the fee is 3%, but your card gives 2% cash back, the net cost is only 1%—which is still worth it for the 18 months of flexibility.

If you get approved for a $3,000 limit but owe $5,000, simply pay the first $3,000 with the card and put the remaining $2,000 on the hospital’s payment plan. You still get the benefits for the majority of the bill.

Applying for the card will cause a small, temporary dip (5-10 points). Adding a large balance will increase your utilization, which might lower your score temporarily. However, as you pay it down, your score will recover.

If you still have a balance when the 0% period ends, you will start paying the standard interest rate (usually 20%+) on the remaining balance. This is why setting up an automatic payment plan for yourself is crucial.

Yes. Dentists rarely offer long-term payment plans. A 0% APR card is often the only way to pay for implants or dentures over time without interest.

Find the Best Credit Card Rates (Compare safer, smarter ways to pay for your healthcare needs.)