The headlines are right: auto insurance rates are rising across the U.S. But here is the most important truth for you and your family: As an experienced driver (ages 50–70), you should be paying significantly less than the national average.

Why? Because insurance costs are primarily driven by risk—and your long, clean driving history and low annual mileage are your most valuable assets.

This guide interprets the latest national data to show you exactly where the savings are and how to claim them. We focus on affordability, security, and using your maturity to your financial advantage.

Key Takeaways: Your Advantage in 2025

- National Average: The national average is $2,301 for full coverage. You should target premiums closer to $2,000 or less.

- Age is a Benefit: Drivers in their 50s and 60s often receive the lowest rates of any age group due to low risk and experience.

- Biggest Savings Lever: The Low-Mileage Discount is your single greatest tool for reducing premium costs in retirement.

- Stability Check: Always verify an insurer’s financial health and low complaint index to ensure peace of mind during a claim.

Your Senior Driver Advantage: Why You Pay Less

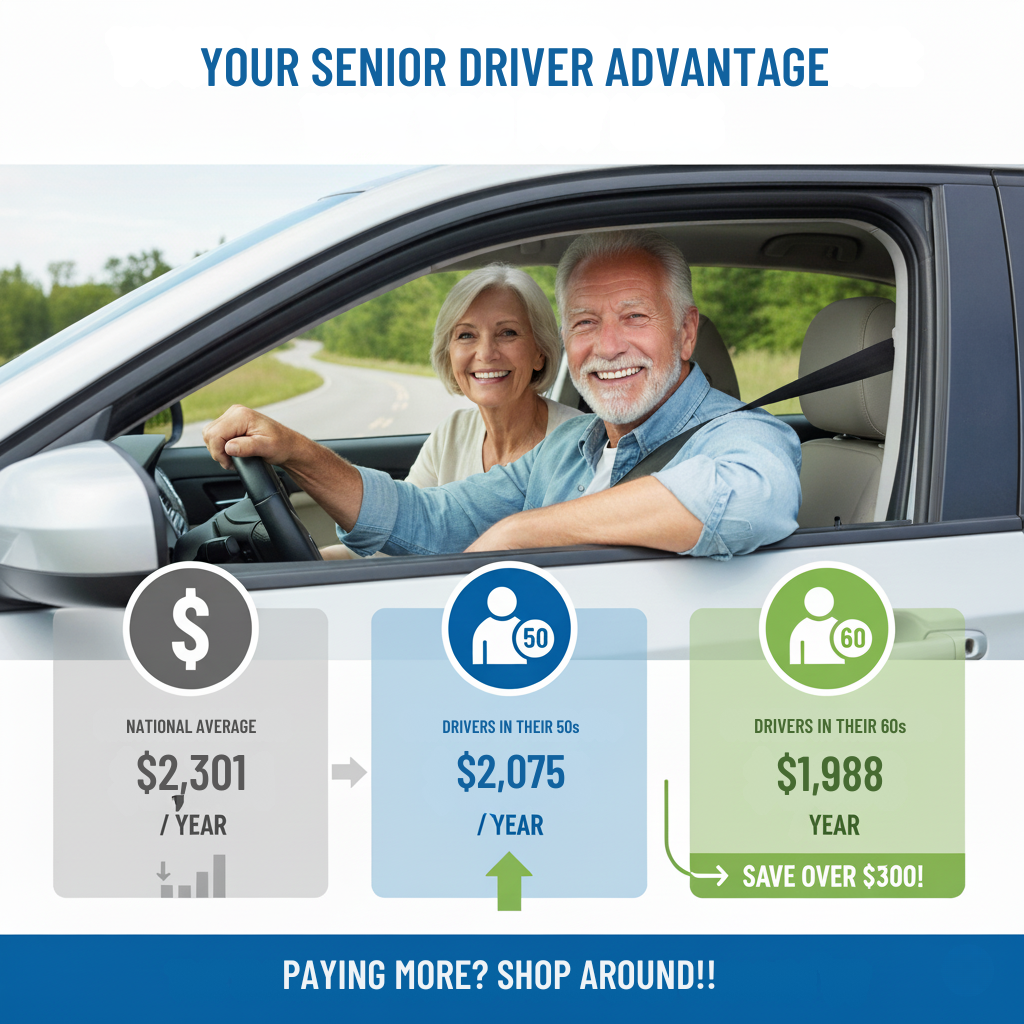

The most important data point in your search is not the national average rate ($2,301/year), but the rate for your specific age group.

Drivers in their 50s and 60s consistently see the lowest rates across the industry. For instance, the median annual full coverage rate drops to just $2,075 for a 50-year-old and even lower, to $1,988 for a 60-year-old—a savings of over $300 compared to the national average.

This reduction is not automatic; it is a reward based on three key factors that define the mature driver:

- Years of Experience (Lower Risk): Insurers view drivers with decades of experience and clean records as the safest demographic on the road, less likely to engage in speeding or severe collisions. This translates directly into the lowest premiums.

- Clean Record Rewards: This age group has had time for youthful tickets or minor accidents to fall off their driving record (typically after 3–5 years), eliminating costly surcharges.

- Discount Eligibility: You are now eligible for Mature Driver and Low-Mileage discounts—savings unavailable to younger drivers—which stack to push your premium down further.

The Takeaway: If you are paying significantly more than the rate shown for your age, it is a strong signal that you are overpaying and should shop around to claim the savings your experience has earned.

Cheapest Companies for Experienced Drivers

While every insurer prices your policy differently, certain companies consistently offer the best value for safe, experienced drivers.

Based on national average rate data, these companies are often the most budget-friendly options for full coverage:

|

Company

|

Median Annual Full Coverage Rate

|

Sagewise Insight for Seniors

|

|---|---|---|

The Cost of Credit: Protecting Your Fixed Income

In most states, insurance companies use a credit-based insurance score to predict the likelihood of future claims. For seniors on a fixed income, this score is critical because the penalty for a lower score can be severe.

Data Callout: For drivers with a clean record, having poor credit results in an average full coverage rate of $3,850 per year—a massive $1,549 annual penalty compared to those with good credit.

Understanding Your Insurance Score

Your insurance score is not the same as your regular FICO credit score, but it draws on the same information: your payment history, amounts owed, and length of credit history. Insurance companies look at patterns of financial management, assuming responsible behavior translates to lower risk on the road.

States That Protect You from Credit Scores

If you live in one of the following states, your credit score cannot be used to determine your auto insurance rates, which may result in significant savings if your score is currently low:

- California

- Hawaii

- Massachusetts

- Michigan

Action Tip: How to Improve Your Score (And Lower Your Premium)

Improving your credit-based score takes time, but it is one of the most effective ways to lower your premium. Focus on these simple actions:

- Pay Bills on Time: This is the single largest factor. Set up autopay for at least the minimum amount due to avoid late payments.

- Keep Balances Low: Avoid using more than 30% of your available credit limit on any revolving accounts (like credit cards).

- Check Your Report: Obtain your free annual credit reports and dispute any inaccuracies immediately.

- Shop Strategically: Some carriers are more forgiving of lower scores than others. Comparing quotes is essential to find the company that weights credit the least.

Your 60-Second Policy Checkup (Are You Over-Insured?)

Use this quick assessment to identify immediate areas where you can cut costs and ensure your liability protection is adequate.

|

Question

|

Yes

|

No

|

Action Path if YES

|

|---|---|---|---|

|

|

|

||

|

|

|

Contact your agent immediately to apply the Low-Mileage Discount.

|

|

|

|

|

||

|

|

|

Smart Strategies to Save Hundreds on Your Policy

1. Deep Dive: The Essential Senior Discounts

Don’t settle for one or two discounts—your history entitles you to stack several for maximum savings. Ensure you check for the following:

- Mature Driver/Defensive Driving: Required in over 30 states for drivers 55+, often netting a 5% to 15% discount for up to three years.

- Low Mileage/Usage-Based: If you drive less than 7,500 miles annually, this is your biggest tool. Pay-per-mile programs (like Nationwide’s SmartMiles) offer up to 40% savings for extremely low-mileage drivers.

- Safety Features: Discounts for anti-lock brakes, anti-theft systems, and passive restraints (like airbags) on your current vehicle.

- Pay-in-Full: A quick discount for paying your 6- or 12-month premium upfront, rather than monthly.

2. The Must-Have Coverage: Uninsured/Underinsured Motorist (UIM)

You may have health insurance, but this coverage is non-negotiable for protecting your assets. It protects you and your passengers when the at-fault driver has either zero insurance (UM) or not enough insurance (UIM) to cover your medical costs, lost wages, and pain and suffering.

- Risk for Seniors: Roughly 1 in 7 drivers nationwide are uninsured. If they hit you, and your medical bills or required lifetime care exceed their state’s low minimum liability limit, UIM coverage steps in to protect your savings from that shortfall.

- The Smart Move: Match your UIM limits to your Liability limits (e.g., $100k/$300k).

3. When to Drop Comprehensive and Collision

As the cost data shows, full coverage (which includes Comprehensive and Collision, or C&C) is nearly four times more expensive than minimum liability.

- Rule of Thumb: If your vehicle is paid off and worth less than $5,000, the cost of your C&C premium plus your deductible may exceed the payout you receive after an accident. This is the time to confidently drop C&C and maintain high Liability Coverage only.

Ready to stop overpaying and lock in your savings?

You’ve earned the right to the lowest possible rate. Our quick comparison tool specializes in matching experienced drivers (50+) with companies that offer the best low-mileage and clean-record discounts.

Frequently Asked Questions (FAQ)

Liability insurance is the barrier between an accident lawsuit and your personal assets. If you cause a serious accident and your limits are too low, the injured party can sue to recover the rest of the damages from your savings, home equity, or future fixed income. Maintaining high limits (e.g., $100k/$300k) is essential for protecting your life’s work.

You should only keep C&C if your car’s market value is substantially higher than the annual cost of the premium plus your deductible. If your car is older and worth less than $5,000, the best financial move is usually to drop C&C.

The average rate often creeps up slightly after age 70 because, statistically, drivers in this age group have a higher frequency of certain types of accidents. However, this statistical increase is usually easily offset by the substantial savings earned through your low annual mileage and clean driving history.

In many states, insurers offer better rates to married individuals. If your marital status has recently changed to widowed or divorced, your rate may unfortunately increase slightly. This is one of the most critical times to shop aggressively, as the penalty varies wildly by company.

You can verify their stability in two ways: check their A.M. Best rating (which assesses their financial strength—aim for “A” or higher), and review their consumer complaint history using the NAIC (National Association of Insurance Commissioners) index. A low complaint index means a simpler claims process.