As we navigate the 2026 financial landscape, most seniors are watching interest rates for one reason: to see how much they’ll pay on their credit cards or earn in their savings accounts. But for those considering a Reverse Mortgage (HECM), interest rates play a much more aggressive and “stealthy” role. In the world of HUD-backed loans, there is an inverse relationship that serves as the foundation of your retirement liquidity: When the “Expected Interest Rate” goes up, the amount of cash you can access goes down.

As your SageWISE Financial Bodyguard, I want to focus on the current math of the 2026 market. We aren’t here to predict the future, but we must audit the present. In the current interest rate environment, many seniors are finding that they are being offered significantly less than they were just a year ago—not because their home value dropped, but because the interest rate “Pivot” shifted the HUD calculation. This blog is your technical audit of the Principal Limit (PL) and why “locking in” your rate is the ultimate defensive maneuver for your 2026 budget.

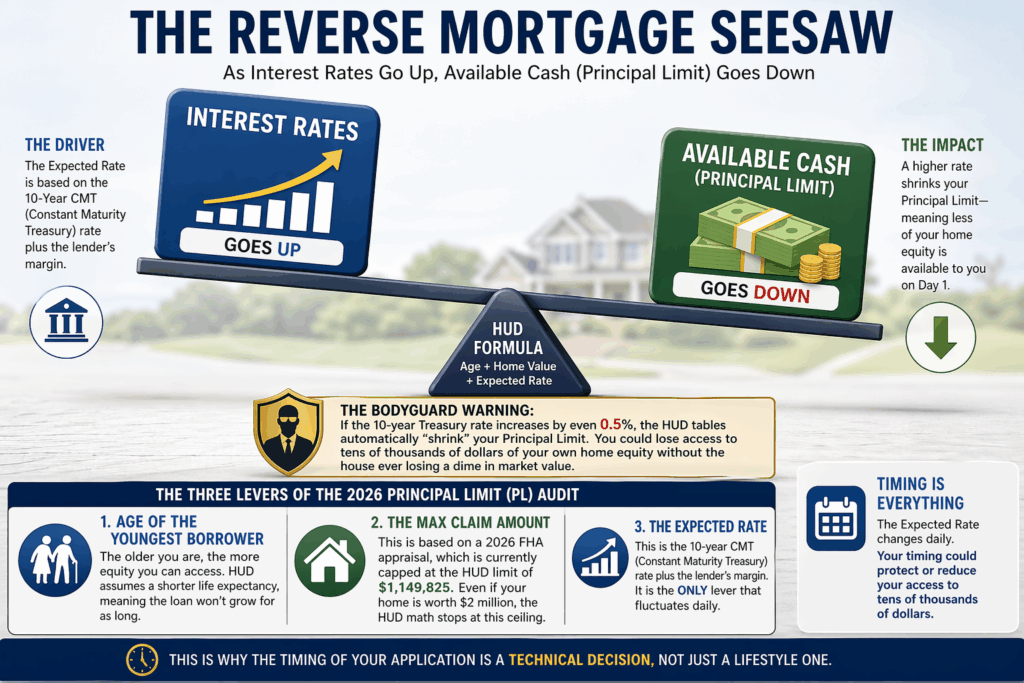

Understanding the "Principal Limit" Mechanics

In a standard “forward” mortgage, a higher interest rate simply means a higher monthly payment. But since a Reverse Mortgage has no monthly mortgage payments, the IRS and HUD have to account for the interest growth differently. They do this by limiting how much of your home’s value you can touch on Day 1. This “bucket” of available cash is your Principal Limit (PL).

The Three Levers of the 2026 PL Audit:

- Age of the Youngest Borrower:

The older you are, the more equity you can access. HUD assumes a shorter life expectancy, meaning the loan won’t grow for as long. - The Max Claim Amount:

This is based on a 2026 FHA appraisal, which is currently capped at the HUD limit of $1,149,825. Even if your home is worth $2 million, the HUD math stops at this ceiling. - The Expected Rate:

This is the 10-year CMT (Constant Maturity Treasury) rate plus the lender’s margin.

The Warning: In 2026, the “Expected Rate” is the only lever that fluctuates daily. If the 10-year Treasury rate increases by even 0.5%, the HUD tables automatically “shrink” your Principal Limit. You could lose access to tens of thousands of dollars of your own home equity without the house ever losing a dime in market value. This is why the timing of your application is a technical decision, not just a lifestyle one.

Strategic Maneuver: Locking the "Floor" in a Volatile Market

In 2026, the market is characterized by a “Pivot” in Federal Reserve policy. Rates are no longer predictably low. To protect your retirement liquidity, you must utilize the Rate Lock Shield.

When you begin your Reverse Mortgage application and pass your mandatory SageWISE Counseling Audit, your lender has the ability to “lock” the Expected Rate. This effectively freezes the HUD math at that moment. If rates spike while your loan is in the 30-to-45-day underwriting process, your cash amount is protected. However, if rates happen to drop during that time, most 2026 contracts allow you to “float down” to the better rate. It is a “heads you win, tails you don’t lose” scenario that every senior should demand.

Bodyguard Tip: Use the Home Equity “Cash Unlock” Calculator to see how much your current home value translates into actual liquid cash at today’s specific 2026 rates.

Table: The 2026 Interest Rate Impact Audit

|

Expected Rate

|

Home Value

|

Age of Borrower

|

Available Cash (Principal Limit)

|

|---|---|---|---|

|

4.5%

|

$500,000

|

72

|

**~$215,000**

|

|

5.5%

|

$500,000

|

72

|

**~$185,000**

|

|

6.5%

|

$500,000

|

72

|

**~$155,000**

|

Why 2026 is the "Liquidity Window" for Seniors

Many seniors are waiting for home prices to climb even higher before they tap their equity. From a technical standpoint, this is a gamble. In 2026, we are seeing “Price Flattening” in many metropolitan markets. If your home value stays flat but interest rates rise, your net borrowing power is actually decreasing.

By acting now, you are essentially “locking in” a portion of your home’s value at today’s rates while retaining full ownership and the right to live in the home. If you wait and rates continue to climb toward 7% or 8%, the HUD “Principal Limit Factors” (the percentages used to calculate your cash) may become so restrictive that the loan no longer meets your needs.

The “Mortgage-Free” Audit: If you are still carrying a traditional mortgage with monthly payments, a high-interest environment makes it even harder to switch to a Reverse Mortgage. Why? Because you must have enough “Principal Limit” to pay off that existing debt in full at closing. If the math doesn’t “clear” because rates are too high, you’re stuck with that monthly payment.

- Action: Check your standing with the Mortgage-Free Planner to ensure you have enough equity to “kill” your monthly payment at current 2026 rates.

The Secondary Shield: Protecting Your "Aging-in-Place" Budget

A Reverse Mortgage in 2026 isn’t just about getting a lump sum of cash; it’s about funding the high cost of modern care. The cost of professional nursing help is at an all-time high.

If you lock in a high Principal Limit today, you can leave that money in a HECM Line of Credit. This is the ultimate “Bodyguard” move because the unused portion of your line of credit grows every month at the same interest rate as your loan. You are essentially turning your home into a “Growth Account” that you can tap for medical needs without ever having to make a payment.

- Planning Tool: Use the Aging-in-Place Budgeter to see how much of a line of credit you’ll need to cover 24/7 care in your own home.

- LTC Costs: Pair your budget with the Long-Term Care Cost Finder to identify the localized costs of care in your zip code for 2026.

Frequently Asked Questions (FAQ)

If you have a variable-rate HECM, your interest will accrue more slowly, which is a win. However, it won’t change your initial Principal Limit. You would need to “Refinance” the HECM (see Blog #6 of this series) to access more cash.

No. The Expected Rate is only used to determine your initial “bucket” of money. Once you close, your actual interest accrues based on a different rate (often the 10-year CMT or SOFR plus a margin).

Indirectly. If rates are high, fewer buyers can afford homes, which can lower comparable sales in your area. This is another reason to audit your equity now.

Yes, but HUD rules require you to take the entire amount as a Lump Sum at closing. This is often a “Financial Mistake” for 2026 seniors because it limits your total borrowing power compared to a variable-rate line of credit.

Use the Home Equity “Cash Unlock” Calculator. It uses current 2026 HUD tables to give you an accurate estimate.

No. Reverse Mortgage proceeds are considered a “loan,” not income. They are 100% tax-free and invisible to the Social Security Administration.

Financial Bodyguard Resources

- Mortgage-Free Planner:

See if you can eliminate your current monthly payment at today’s rates. - Aging-in-Place Budgeter:

Calculate the cost of staying in your home vs. moving to a facility. - Home Equity “Cash Unlock” Calculator:

Audit your 2026 Principal Limit before the next rate hike.

Final Tax Audit

In 2026, the greatest threat to your home equity isn’t necessarily a market crash—it’s an interest rate spike that limits your access to that equity. By auditing your Principal Limit today and understanding the technical mechanics of the HUD “Expected Rate,” you can lock in your financial independence while the window is still open. Don’t let your “Invisible Equity” remain trapped by outdated math.