One of the most persistent fears seniors have about annuities is the “Vanishing Principal” myth. You’ve probably heard the horror stories: “Don’t buy an annuity! If you die tomorrow, the insurance company keeps every penny of your money!”

This fear keeps thousands of retirees from securing the guaranteed income they desperately need. They choose to stay in the volatile stock market because they want to “leave something for the kids,” unaware that the market’s downside poses a much greater threat to that legacy than an insurance contract ever would.

But here is the sageWISE Security Update: In 2026, most modern annuities are built with “Legacy Guardrails.” You can guarantee a paycheck for life while ensuring that every unused dollar of your principal goes directly to your heirs—bypassing the slow, expensive probate court system.

As your trusted advocate, we have performed a Sagewise Audit of annuity death benefits. We will show you the “Cash Refund” secret, explain how to avoid the “Inherited IRA Tax Trap,” and provide the FAQs you need to ensure your “Income Shield” doesn’t become a “Legacy Leak.”

Key Takeaways

- The Probate Bypass: Annuities are insurance contracts. They pay directly to named beneficiaries, usually within 7 to 10 days, avoiding the 12-month probate wait.

- Standard vs. Enhanced: Every annuity has a standard death benefit, but you can buy “Enhanced” riders that grow your legacy even if you spend your cash.

- The Refund Rule: Always look for a “Cash Refund” or “Installment Refund” feature. This ensures the insurance company never “keeps the change.”

- The Tax Reality: Heirs generally pay ordinary income tax on the gains of the annuity, but the principal is returned tax-free.

Protect your family’s inheritance while securing your own income.

Get Your Free, Personalized Annuity Quote

The sageWISE Audit: How Death Benefits Actually Work

To be your own financial bodyguard, you must understand that an annuity death benefit is a “Contractual Guarantee” that overrides your Will. It doesn’t matter what your lawyer wrote in your testament; the insurance company will only send money to the names listed on your Beneficiary Form.

1. The Standard Death Benefit (The Baseline)

If you die before you start taking “Annuitized” income, your heirs typically receive the full Account Value. This includes your original deposit plus any interest earned, minus any withdrawals you took for living expenses.

- The Benefit: It is simple and automatic.

- The Risk: If the stock market is down (in a Variable Annuity) or if you’ve spent most of your cash, there may not be much left for the kids.

2. The "Return of Premium" Shield

Many seniors choose a Fixed Index Annuity (FIA) with a “Return of Premium” rider.

- How it works: No matter how much money you withdraw for your own needs, the insurance company guarantees that your heirs will receive at least the original amount you deposited.

- The Math: You deposit $200,000. You spend $150,000 over 20 years. You pass away with only $70,000 left in cash. Under this shield, the company pays your heirs the full **$200,000**. They essentially “insure” your principal for the next generation.

Annuity Payout Estimator

How much of a legacy can you actually leave behind while still funding your own life? Use our Annuity Payout Estimator to calculate how much guaranteed income your current savings can generate and see the estimated “Death Benefit” balance for your heirs.

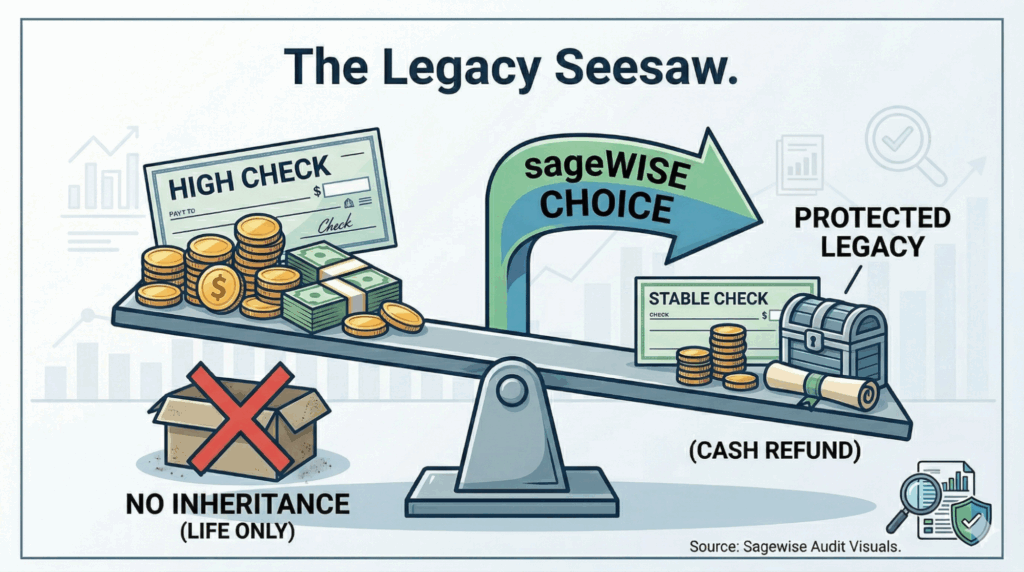

The "95% Protection" Trap: Why "Life Only" is Dangerous

If you are searching for “highest annuity payout rates,” you will see a payout option called “Life Only.” * The Seduction: This pays the absolute highest monthly check. A 70-year-old might get $850/mo on $100,000.

- The Danger: This is the only version where the insurance company “keeps the change.” If you die in month three, the checks stop and your heirs get $0.

- The Bodyguard Fix: Never choose “Life Only” unless you have no heirs and no interest in a legacy. Instead, demand a “Life with Cash Refund” option. Your monthly check will be slightly smaller (e.g., $780 instead of $850), but the bank is legally obligated to return any unused principal to your family.

Inheriting an Annuity: The "10-Year Rule" Warning

If your children inherit your annuity, they don’t just get a “gift”; they get a tax responsibility. Just like an Inherited Gold IRA, annuities follow strict IRS distribution rules.

- Non-Qualified Annuities (Bought with Cash): Heirs usually choose the “Five-Year Rule” (take it all in 5 years) or the “Life Expectancy” option (take it over their lifetime).

- Qualified Annuities (Bought with IRA money): Under the SECURE Act, most non-spouse heirs must empty the account within 10 years.

- The sageWISE Tip: If your heirs are in their peak earning years, taking a $100,000 annuity payout all at once can push them into a 37% tax bracket. Encourage them to use the “Stretch” or “10-Year” window to take smaller amounts and minimize the IRS bill.

Frequently Asked Questions (FAQ)

Yes. This is called “Spousal Continuation.” Your spouse can step into your shoes, keep the contract active, and continue receiving the income or letting the money grow tax-deferred. It is the smoothest wealth transfer in the financial world.

They serve different purposes. Life Insurance pays a large, tax-free lump sum for a relatively small premium. An annuity is for income while you are alive, with the death benefit acting as a “backup” to protect your unused principal. For maximum protection, we suggest having both.

No. The annuity death benefit is cash paid to your beneficiaries. They can use that cash to pay property taxes, insurance, or funeral costs, but the annuity itself has no connection to your home’s liability.

This is a popular add-on for Fixed Index Annuities. The company guarantees that your “Legacy Value” will grow by a set percentage (e.g., 5% compound) every year, regardless of what you spend or how the market performs. It effectively turns your annuity into a “hybrid” between an income plan and a life insurance policy.

You simply put the charity’s legal name and Tax ID (EIN) on the beneficiary form. This is a very smart move for high-net-worth seniors, as charities pay $0 in taxes on annuity gains, ensuring 100% of your gift is used for the cause.

Get Your Free Annuity Quote (Audit your legacy plan. Secure your heirs’ future today.)