You have spent 40 years playing by the rules. You saved diligently in your Gold IRA, you paid off your mortgage, and you’ve built a nest egg designed to last the rest of your life. You are, by all definitions, “High-Net-Worth”—even if you don’t feel like a millionaire. If you own a home with $400,000 in equity and have $600,000 in retirement accounts, you have a million-dollar target on your back every time you pull out of your driveway.

But here is the sageWISE Warning: Your “Full Coverage” auto insurance policy has a ceiling that is likely far lower than your total net worth.

In 2026, a single multi-vehicle accident or a serious injury to a pedestrian can result in a legal judgment exceeding $1 million. If your auto policy caps out at $250,000 or $500,000, your personal assets—the very foundation of your retirement—are the “Secondary Payer” for the remaining balance. Without an Umbrella Policy, you are effectively self-insuring your life’s work against the mistakes of a single split-second.

As your trusted advocate, we have performed a Sagewise Audit of the “Liability Gap.” We will show you the math of the “Targeted Retiree,” explain why Umbrella insurance is the cheapest “Legacy Shield” you can buy, and provide the exact steps to anchor your protection today.

Key Takeaways

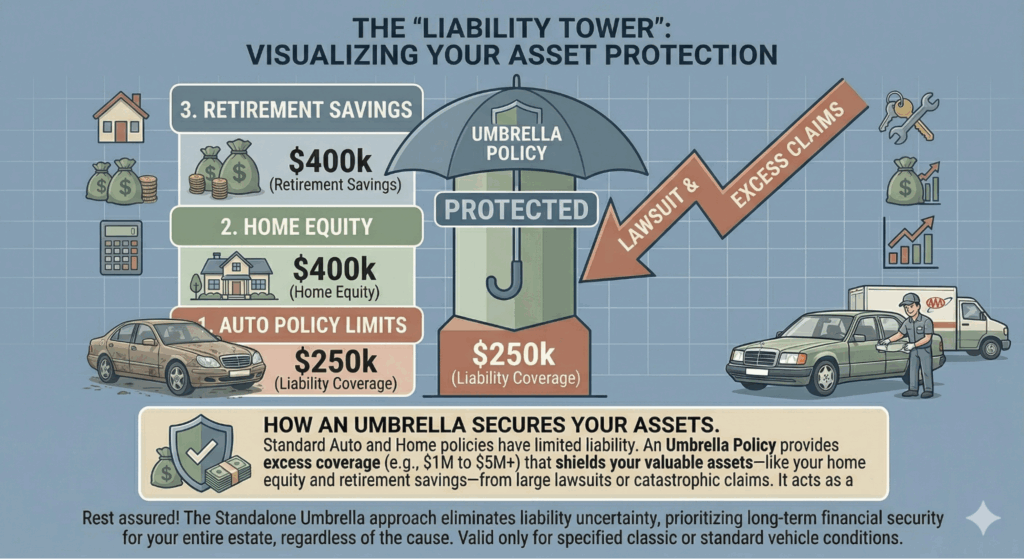

- The Liability Gap: If a lawsuit exceeds your auto limits, a judge can order the liquidation of your non-retirement assets to pay the debt.

- The Umbrella Function: It sits on top of your home and auto policies, providing an extra $1 million to $5 million in protection.

- The Cost-to-Value Ratio: For most seniors, a $1 million Umbrella policy costs less than **$20 a month**.

- Legal Defense Included: One of the greatest “hidden” benefits is that the insurance company pays 100% of your legal defense fees, which can exceed $50,000 in a major case.

- The sageWISE Tip: You must increase your underlying auto limits (usually to 250/500) before a company will sell you an Umbrella “Anchor.”

Stop gambling with your retirement savings. See if your current rates are “Market Fair” before you add your liability shield.

Check Your New Senior Rate Now

The sageWISE Audit: Identifying the "Target" on Your Back

In the legal world, there is a term called “Deep Pockets.” Personal injury attorneys don’t just sue for the fun of it; they sue people who have assets that can be seized.

1. The "Million-Dollar" Accident Math

Imagine you are driving to the grocery store. A light turns yellow, you misjudge the distance, and you collide with a minivan. Two people are injured, requiring surgeries and long-term physical therapy.

- Your Auto Limit: $250,000 per person / $500,000 per accident.

- The Legal Judgment: $1,200,000 (Medical bills + Lost wages + Pain and suffering).

- The Gap: $700,000.

The Consequence: Because you have no Umbrella policy, the plaintiff’s attorney will look at your home equity and your non-ERISA brokerage accounts. They can place a lien on your home or garnish your Annuity payouts. You are forced to pay for a split-second mistake with your entire retirement future.

2. The "Pedestrian" Risk

Seniors are often involved in low-speed accidents in parking lots or residential areas. If you accidentally strike a pedestrian, the medical bills for a broken hip or head injury in 2026 can easily cross the $500,000 mark before the case even reaches a courtroom.

How the Umbrella Policy Acts as an "Anchor"

An Umbrella policy is not a standalone product; it is a “Follow-Form” coverage. It coordinates with your primary policies to create a seamless wall of protection.

- Exhaustion of Primary Limits: Your auto insurance pays out its maximum (e.g., $250,000).

- The Umbrella Drops: The moment that limit is hit, the Umbrella policy opens. It covers the remaining amount up to your chosen limit (usually $1M or $2M).

- Global Protection: Unlike your car insurance which only covers driving, or your home insurance which only covers your property, an Umbrella policy follows YOU anywhere in the world. If you are sued for a “slip and fall” at a vacation rental in Europe or an incident involving your dog at a park, the Umbrella anchor keeps your assets safe.

The Math: The Cheapest $1 Million You'll Ever Buy

Retirees are often hesitant to add “another bill” to their budget. But from a Financial Bodyguard perspective, the math of an Umbrella policy is the most logical “Buy” in the insurance industry.

|

Coverage Amount

|

Average Annual Cost

|

Monthly Budget Impact

|

|---|---|---|

|

$1 Million

|

$180 - $250

|

**~$18.00**

|

|

$2 Million

|

$280 - $350

|

**~$27.00**

|

|

$5 Million

|

$500 - $700

|

**~$50.00**

|

The sageWISE Verdict: You are paying roughly $0.60 a day to protect a lifetime of savings. This is significantly cheaper than the Loyalty Tax most seniors pay on their standard policies without even realizing it.

Step-by-Step: How to Audit and Secure Your Shield

Don’t wait for a process server to knock on your door. Follow this roadmap to secure your retirement today.

Step 1: Calculate Your "Asset exposure"

Add up your home equity, your savings accounts, and your non-retirement brokerage accounts. (Note: In many states, 401ks and IRAs have some protection, but home equity is a primary target). If the total is over $300,000, you need an Umbrella.

Step 2: Use the "Senior Driver Discount Finder"

To qualify for an Umbrella, your insurer will require you to raise your auto liability limits to 250/500. This will increase your auto premium slightly. Offset this cost by finding every hidden senior credit you are entitled to.

Open Senior Driver Discount Finder

Step 3: Run the "Rate Estimator"

If your current “Captive” company (like State Farm or Allstate) quotes you a high price for the Umbrella and the limit increase, they may be practicing Price Optimization on you. Use our tool to find a “New Business” rate that includes the higher limits for less than you pay now.

Open Car Insurance Rate Estimator

Step 4: Contact an Independent Broker

As we detailed in our Independent Broker Edge guide, brokers have access to “Standalone Umbrella” carriers (like RLI). This allows you to keep your house and car with different companies while still having a single umbrella that covers both.

Quick Comparison: Standard Liability vs. Umbrella Shield

|

Feature

|

Standard Auto Policy

|

With Umbrella Anchor

|

|---|---|---|

|

Max Payout

|

$250,000 - $500,000

|

**$1.5 Million - $5.5 Million**

|

|

Personal Assets at Risk

|

HIGH (If judgment > limit)

|

ZERO (In most cases)

|

|

Legal Defense Costs

|

Stops when limit is hit.

|

Insurance pays until case is over.

|

|

Coverage Scope

|

Driving only.

|

Worldwide / All Activities.

|

|

Verdict

|

Basic Compliance

|

Retirement Security

|

Frequently Asked Questions (FAQ)

Yes. As we noted in our Inherited Property Sharks guide, a standard Living Trust protects your heirs from probate, but it does not protect you from personal liability while you are alive. A judge can still order the trust assets to be used to satisfy a judgment.

It is difficult but possible. Most “Anchor” policies require you to have at least one primary policy (Auto or Home) with a certain level of liability. If you rent, your Renters Insurance serves as the primary base for the Umbrella.

Yes! This is a unique benefit for seniors active on social media or in community boards. If you are sued for something you wrote in a “Nextdoor” group or a local review, your auto insurance won’t help—but your Umbrella Shield will provide your legal defense.

As discussed in our Snowbird Guide, an Umbrella policy is the perfect solution for multi-state living. It provides a single, unified layer of protection that covers you regardless of which car you are driving or which state you are in.

Generally, no. For a personal primary residence and personal vehicles, the premium is a non-deductible personal expense. However, if you own rental properties that are also covered by the umbrella, a portion of the premium may be deductible as a business expense.

Check Your New Senior Rate Now (Protect your legacy. Anchor your retirement with a liability shield today.)