You’ve just stepped off a long flight to visit your grandkids. You’re tired, you’re carrying heavy bags, and you just want to get to your hotel. You reach the rental car counter, and the agent begins the “Safety Interrogation.”

“Do you want to add our full coverage for $29.99 a day? If you don’t, and there is even a scratch on this car, you could be responsible for the full value of the vehicle plus the loss of our daily revenue while it’s in the shop.”

It is a high-pressure pitch designed to trigger a fear-based decision. For a senior on a fixed income, an extra $210 on a week-long rental is a significant “Vacation Tax.”

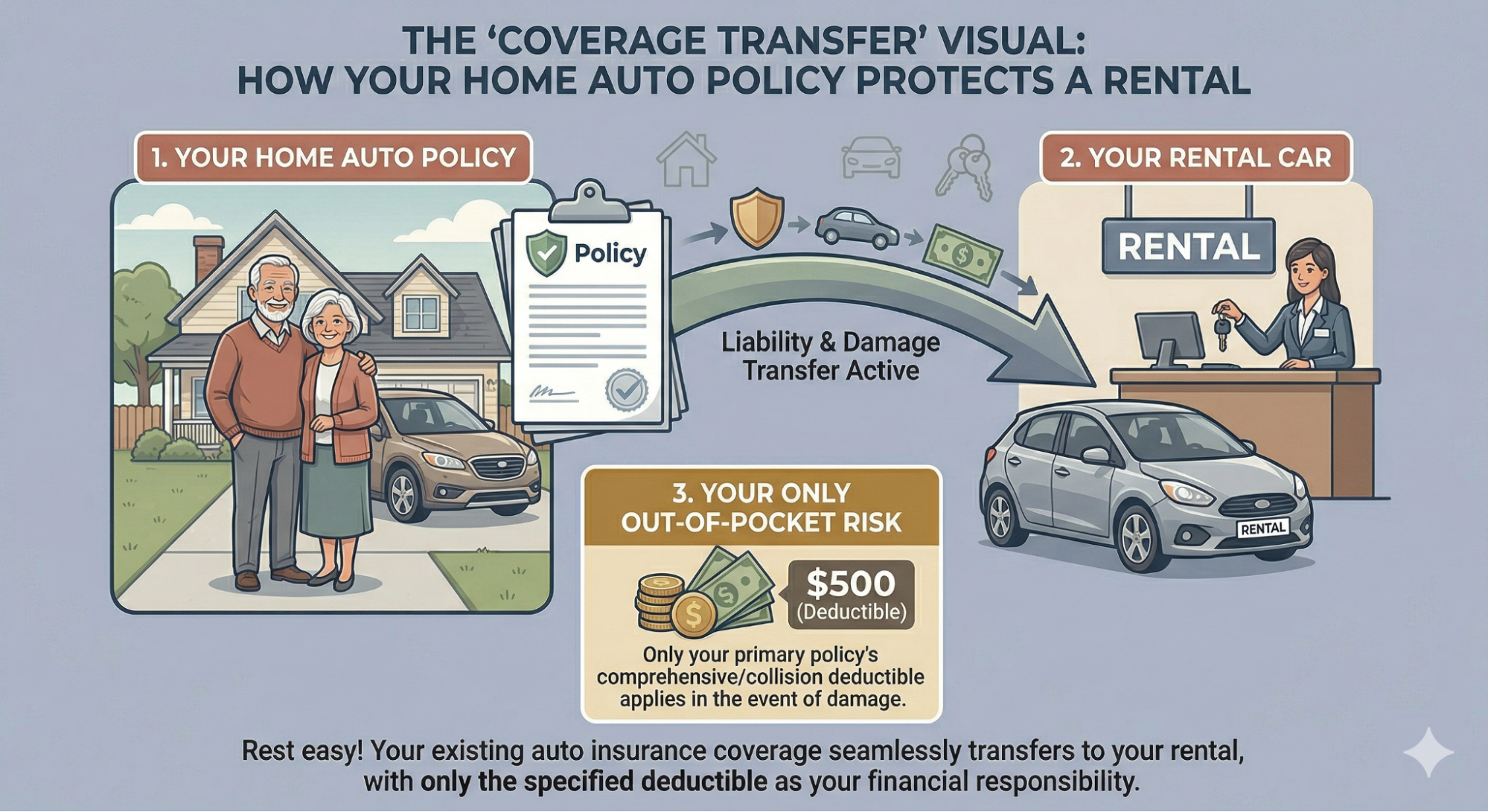

But here is the sageWISE Warning: Buying insurance at the rental counter is often like buying a second roof for a house that is already fully covered.

Most seniors are already carrying Triple-Layer Protection in their wallets, but they don’t know how to activate it. As your trusted advocate, we have performed a Sagewise Audit of the 2026 rental car landscape. We will show you the math of the “Counter Markup,” explain the difference between primary and secondary coverage, and give you the exact script to use to decline the upsell with confidence.

Key Takeaways

- The Coverage overlap: Your Full Coverage Auto Policy usually follows you into the rental car, covering both liability and physical damage.

- The Credit Card Shield: Most mid-to-high-end credit cards provide a built-in Collision Damage Waiver (CDW) for free, provided you use the card to pay for the rental.

- The “Loss of Use” Trap: This is the one thing the rental company can charge you for that your personal insurance might not cover. We’ll show you how to audit this risk.

- The sageWISE Tip: Never buy rental insurance until you’ve checked your Senior Driver Profile. If you’ve used our Senior Driver Discount Finder, you may already be in a “Preferred” tier that includes rental perks.

Stop the counter-shaming. See if you are overpaying for your total insurance package today. Check Your New Senior Rate Now

The sageWISE Audit: The Math of the "Counter Markup"

To be your own financial bodyguard, you must understand that the rental counter is a retail environment, not a medical or safety clinic. Insurance products (CDW, SLI, PAI) are the highest-margin items the rental company sells.

Scenario: A 7-Day Rental of a Standard SUV.

|

Protection Layer

|

Daily Cost

|

Total Trip Cost

|

Why It's Often Unnecessary

|

|---|---|---|---|

|

Collision Damage Waiver

|

$29.99

|

**$209.93**

|

Already covered by your Comprehensive/Collision limits.

|

|

Supplemental Liability

|

$14.95

|

**$104.65**

|

Already covered by your home/auto Umbrella Policy.

|

|

Personal Accident

|

$6.00

|

**$42.00**

|

Already covered by your Medicare or Health Insurance.

|

|

TOTAL UPSELL

|

$50.94

|

$356.58

|

Nearly doubles the price of the rental.

|

The Audit Result: For most seniors, that $356 is a “Loyalty Tax” to a rental company for protection they already own. By using our Car Insurance Rate Estimator, you can verify that your current premiums already include “Temporary Substitute Vehicle” coverage, making the counter insurance redundant.

Layer #1: Your Personal Auto Policy (The Primary Shield)

In the United States, your personal auto insurance policy is portable. It doesn’t just cover your 2018 Toyota in your driveway; it covers YOU as a driver.

- Liability Transfer: If you hit someone while driving a rental car, your personal policy’s Bodily Injury and Property Damage limits step in first. As we noted in our Uninsured Motorist Audit, your high limits are your best defense against a lawsuit.

- Physical Damage Transfer: If you carry “Full Coverage” (Collision and Comprehensive), those coverages transfer to the rental car. If you wreck the rental, your insurance pays the rental company the Actual Cash Value of the car, minus your deductible.

- The Deductible Risk: This is the only “leak” in this shield. If you have a $500 deductible, you will have to pay that $500 to the rental company if you crash.

Layer #2: Your Credit Card (The Secondary Shield)

If you pay for the rental using a credit card like the Chase Freedom Unlimited or the Amex Blue Cash Everyday, you likely have a built-in “Auto Rental Collision Damage Waiver.”

- Secondary Coverage: Most cards are “Secondary.” This means if you crash, they pay your $500 personal insurance deductible and any “towing fees” the rental company charges. It essentially makes your personal claim “Zero Cost” to you.

- Primary Coverage: Some premium cards (like Chase Sapphire Preferred or the Bilt Mastercard) offer “Primary” coverage. This is the Gold Standard. If you have a wreck, they pay for the whole car and you never even have to tell your personal insurance company. This prevents a Claim Surcharge on your home policy.

The “Must-Do” Step: To activate this shield, you MUST decline the rental company’s CDW. If you accept their insurance, your credit card coverage is automatically voided.

The "Loss of Use" Trap: The One Reason to Be Cautious

We are honest brokers: there is one legitimate “Anxiety Hook” the rental agent will use. It’s called Loss of Use.

If you wreck a rental car and it sits in a body shop for 10 days, the rental company will charge you for the 10 days of “lost revenue” because they couldn’t rent that car to someone else.

- The Problem: Many personal auto insurance policies do not cover “Loss of Use.”

- The Math: If the car’s daily rate is $50, you could owe a $500 “Administrative Fee” for the downtime.

- The sageWISE Fix: Before you travel, call your Independent Broker and ask: “Does my policy cover Loss of Use or Diminished Value on a rental car?” If the answer is no, and you are worried about a $500 bill, that is the only reason to consider a third-party rental policy (like Allianz or RentalCover.com), which costs about $9/day—far less than the counter’s $30.

The Counter Protocol: A Senior's Step-by-Step Guide

Don’t let the agent’s script rattle you. Follow this “Financial Bodyguard” roadmap when you reach the front of the line.

Step 1: The "Digital Proof" Preparation

Before you leave home, take a photo of your insurance Declarations Page on your phone. If the agent asks, “Are you sure you’re covered?” you can show them exactly what your limits are.

Step 2: The "Decline" Script

When they ask about the CDW/LDW, use these exact words:

“I decline all optional coverages. I have primary liability through my [Brand] policy and secondary damage protection through my [Visa/Amex] card. I am aware of the ‘Loss of Use’ risk and I accept it.”

Step 3: The "Pre-Existing Damage" Audit

Most rental “scams” happen because of pre-existing scratches. Use your smartphone to record a 30-second video of the car before you leave the lot. Walk around the entire car, focusing on the rims, the windshield, and the roof. This video is your “Defense Shield” if they try to charge you for a dent that was already there.

Comparing Your Options: Rental Counter vs. Alternatives

|

Feature

|

Rental Counter ($30/day)

|

Credit Card ($0/day)

|

Third-Party ($9/day)

|

|---|---|---|---|

|

Ease of Claim

|

Easiest (Walk away)

|

Moderate (Paperwork)

|

Moderate

|

|

Impact on Personal Rate

|

Zero

|

Possible (if secondary)

|

Zero

|

|

Covers "Loss of Use"

|

Yes

|

Sometimes (check terms)

|

Yes

|

|

Covers International

|

No (varies)

|

Often Yes

|

Yes

|

|

Bodyguard Verdict

|

Expensive Overkill

|

Best for US Travel

|

Best for Europe/Mexico

|

Frequently Asked Questions (FAQ)

Yes. As we detailed in our guide on Medicare vs. Auto Insurance, Medicare follows you anywhere in the U.S. You do not need the “Personal Accident Insurance” (PAI) offered at the counter. It is a total duplication of benefits.

Often, no. Many credit card waivers exclude countries like Italy, Ireland, and Israel. If you are traveling internationally, a third-party policy from a company like Allianz is a “Financial Bodyguard” necessity.

Most credit card and personal policies have a Value Cap (often $50,000) and an Occupancy Cap (usually 7-8 passengers). If you are renting a $90,000 Cadillac Escalade or a 12-passenger van, your personal shield may be “Underpowered.” In this specific case, buying the counter insurance is a smart move.

Directly? No. But many seniors use their AARP or AAA memberships to get a 10-25% discount on the base rental rate, which more than covers the cost of a few “Loss of Use” risks.

They are essentially the same. CDW (Collision Damage Waiver) covers accidents. LDW (Loss Damage Waiver) usually covers theft and vandalism as well. Both are waived if you have Full Coverage on your home policy.

Check Your New Senior Rate Now (Protect your vacation budget. Use the shields you already have.)